.jpeg)

Key Takeaways

There is a path that leads RIAs to deeper and more lucrative relationships with their clients by building capabilities over time. It starts with a change in perspective: firms need to move past acting like vendors where they deliver money management to clients at arm’s length. Instead, they need to sit at the same side of the table as their clients, act as trusted advisors that are helping them reduce risks and take advantage of opportunities across their financial, business, and personal activities.

But this broader mindset requires the capacity to deliver a wider range of services with the precision and security that wealthy families demand today. The back-office infrastructure of most RIAs is often bogged down with inefficient manual processes that can barely keep up with their existing business.

This report details four critical steps that RIAs can take to transition to serve clients better and evolve towards a full multi-family office offering. It draws from 15 years of experience of Masttro working with wealthy families and MFOs, and our wealth management platform that was designed from the start to support the exacting requirements of sophisticated family offices.

We’ve seen very successful MFOs that evolved from registered investment advisors and they have one thing in common: a bulletproof information infrastructure is in place for their professionals to earn the trust of wealthy families.

But it starts with a change in perspective.

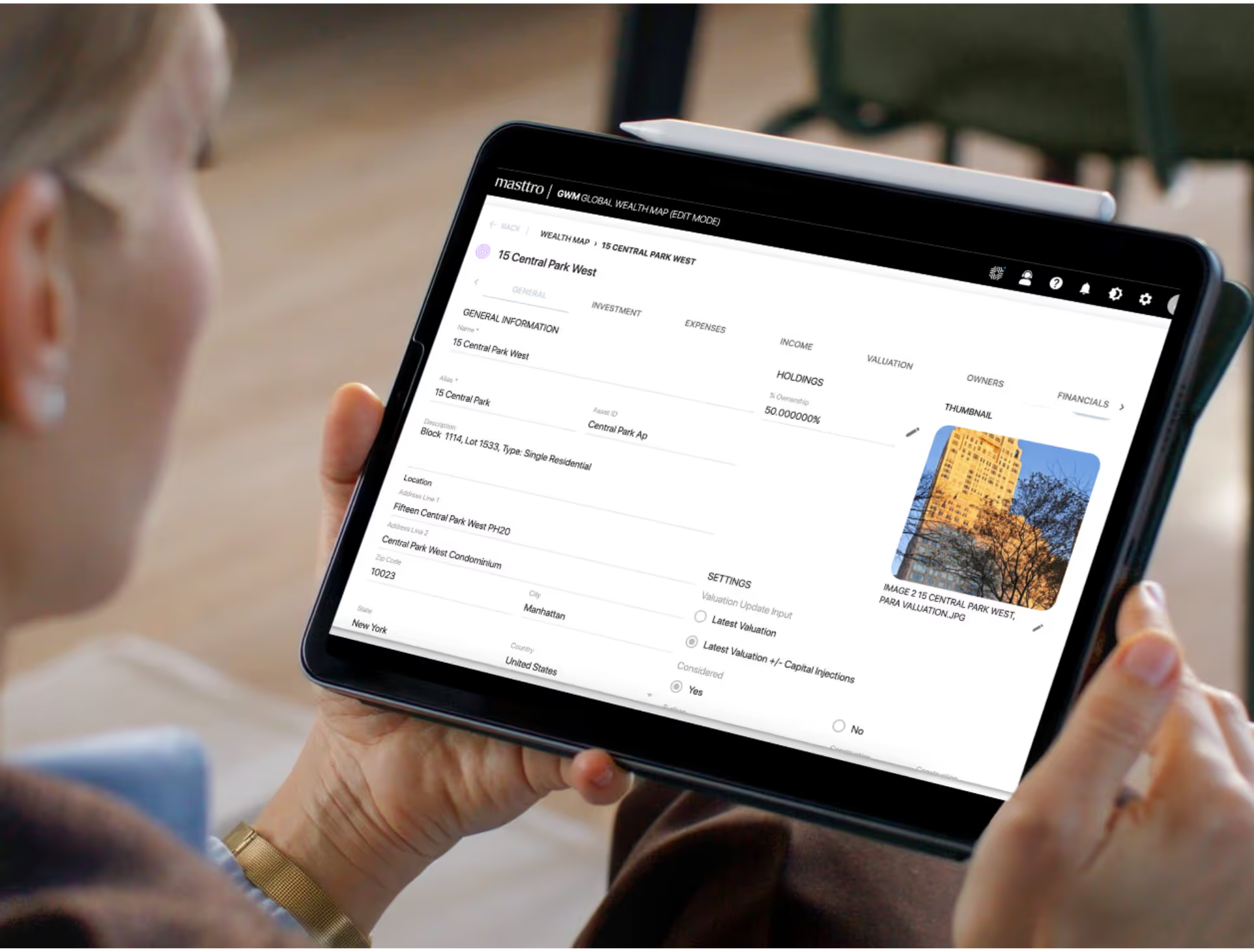

Deliver Better Information

A simple monthly statement sent as a PDF doesn’t cut it anymore. Wealth owners invest around the world and increasingly rely on alternative investment vehicles like private equity funds and real-estate pools. And they expect to have up-to-the-minute information about all their holdings in reach at any time, anywhere.

Most investment advisors are still using systems designed for listed securities, often in a single currency. Sometimes they get electronic data feeds from a single custodian. As their clients’ investment horizons expand, these firms compensate by manually adding below-the-line investments to their statements. Perhaps they use third-party aggregation services to collect some numbers. Each additional step adds effort and makes the information reported older, less detailed, and more likely to hold errors.

All assets

Statements and reports should have the most detailed, up-to-date information on assets of every type in any currency, whether listed securities, private funds, or directly held. Even if you’re just reporting on the investments you manage today, build the capacity to integrate and report on the holdings of other managers and financial institutions. That way, you’re in a position to provide advice on portfolio allocation and cash-flow management, and give an accurate overview across all asset classes.

Perfectly accurate

Every number on every report must be rock solid. Spreadsheets are a magnet for human error. Eliminate manual data entry, spreadsheets, and third-party aggregators. Build direct electronic connections with banks and custodians to guarantee fast and accurate investment information.

Always available

In addition to periodic statements, provide clients with an online portal and a mobile app with access to their portfolio, cash positions, and performance information.

Five Dashboards Every Wealth Owner Needs

Focus on Protection

Clients with substantial assets are often in the public eye and more vulnerable to a wide range of threats. When advisors use a patchwork of systems and vendors for back-office functions, there is added risk that sensitive information could get into the wrong hands.

Similarly, the complex lives and investment portfolios of wealthy families are increasingly straining the ability of many RIAs to diligently follow KYC, anti-money-laundering, and other regulations.

End-to-end security

Data should be encrypted all the way from the source until it reaches the wealth owner or designated advisor. If you rely on a third-party vendor, scrutinize their processes and data protection practices. But preferably don’t. Also: if their fees are based on AUM, it means they have access to your client portfolio data.

Granular permissions

Wealth owners are typically concerned about providing for their family members, but that doesn’t mean they want everyone in the family to see everything in all their portfolios. Build systems that can deliver reports and online access for a subset of accounts to specific family members or outside advisors.

Proactive compliance

Run your business on the assumption that regulatory and compliance regimes will continue to get stricter in every jurisdiction. Ensure your compliance systems have access to all the relevant accounts and transactions. Build alerts that signal when information is missing or needs to be updated. A system that integrates reporting and compliance is the best way to make sure that potential violations don’t fall through the cracks and that there is a detailed audit trail in case questions arise.

Streamline Operations

RIAs can find it hard to keep up with client requests because of slow and inflexible back-office operations. Many of these investment professionals left large financial institutions to escape cumbersome bureaucracy, yet over time they have hired dozens, maybe hundreds, of people to massage data and enter information from printed statements into their systems.

Outsourcing functions like data aggregation and compliance may seem like a way to keep operations lean, but managing these relationships brings its own complexity, as well as the decreased accuracy and increased risk we’ve mentioned.

Direct connections

Ensure that your core data platform can be connected directly to the institutions your clients use or might use in the future. Most large banks and custodians support direct connections, as do an increasing number of private investment managers. For those that don’t, use a system that can automatically extract data from statements. Third-party data intermediaries are prone to data leaks and other risks.

Automatic processing

Look for manual processes throughout your operation that can be automated. Often these include tax reporting, compliance verification, invoicing, and similar functions.

Serve More Client Needs

Once an advisory firm has a platform with quality information, reliable security, and efficient operations, it is better positioned to provide additional services to wealthy families. There isn’t a binary choice between being an RIA or an MFO. Rather, are functions that firms can offer depending on the needs of their clients and their internal capabilities. This might rely on external partners - and the right partners will make all the difference to deliver those services in an integrated, high-quality way. Here’s three complementary services to consider.

Comprehensive reporting

Tallying the holdings of a sophisticated wealthy family is a surprisingly complex task. Not only do they invest in myriad public and private assets around the world, they also spread those holdings among a web of trusts, joint ventures, and other account types. A significant share of the family’s wealth may be in physical assets, from art and jewelry to megayachts and cattle ranches. Information on cash holdings—including expected inflows and outflows—is also essential for wealthy families to plan for expenses and investments. Delivering a comprehensive picture of all of these assets is a valuable service in itself and a foundation for other advisory functions.

Asset and estate advice

The most important leap for most RIAs is to shift from managing a portion of a client’s portfolio to holistically advising them on their entire wealth across generations. An integrated view enables a sophisticated analysis of risk and return. And it creates the opportunity to provide advice on taxes, estate planning, charitable giving, major expenses, and other financial matters.

Administrative services

Investment advisors are well-positioned to assist clients with the complex monitoring and paperwork requirements of their holdings. These can include bookkeeping, accounting, tax reporting, and bill paying. Ultimately, firms may be able to manage and track a wider range of activities, such as aircraft operation, home construction, and automotive fleet coordination.

Conclusion

A full-service MFO offers bespoke solutions to manage the unique problems of the ultra-wealthy.

One day, the challenge could be buying an island to develop a compound on it. The next day, it might be bailing an errant nephew out of jail on the other side of the world. Or creating a well-structured succession plan.

In this report, we’ve argued that registered investment advisors don’t need all these capabilities to escape from the narrowing and competitive world of traditional money management. Indeed, advisors that promise family office services that they can’t deliver put their hard-earned reputations at risk.

Rather, we suggest the best start is to shift their mindset from managing money to solving clients problems. This shift allows firms to provide advice on their clients’ full financial situation and opens the door to offer assistance with other needs.

And we know from long experience that the biggest impediment for most firms trying to make this transition is a back-office infrastructure that can barely keep up with their current business, let alone the increased demands of the wealthy.

It’s why the Masttro platform was designed specifically for the complexities of modern family offices.

Speak to us, and we’ll show you how you can give your clients a complete view of all their holdings. You’ll see we’ve ensured accuracy and security through direct connections to hundreds of institutions. And you can learn how much more productive your firm can be with one system that integrates reporting, risk management, compliance, billing, tax accounting, and many more of the functions that wealthy families expect.

If you are interested in learning more, including working with our team to perform a current-state assessment, develop a target-state blueprint, and more, get in touch at contact@masttro.com.

Give your clients a complete view of all their holdings.